Bioenergy Europe’s Recommendations EU Heating and Cooling Strategy

Bioenergy Europe’s Recommendations for the Heating and Cooling Strategy

Heating is one of the areas where Europe can make faster and more affordable progress on climate action, but only if it is treated as a priority. Now more than ever, it is imperative to rely on local, renewable heat sources that support European manufacturing and innovation, such as sustainable bioenergy. Bioenergy Europe emphasises the need to prioritise clean heat as a vital aspect of the energy transition. It calls on the Commission to incorporate these key points into the upcoming Heating and Cooling Strategy.

Introduce clear trajectories for the phase-out of fossil fuels from the heating and cooling sector.

Problem

The current rate of fossil fuel phase-out is insufficient. Fossil systems are still allowed and supported in several Member States, slowing down decarbonisation pathways in both the building and industrial sectors. Fossil fuels[1] remain dominant, accounting for circa heat consumption. The current efforts are insufficient to deliver the required average annual increase of 1.8 percentage points in renewable heating and cooling (H&C) at the Union level, as foreseen under the Renewable Energy Directive (RED III).[2]

[1] Including non-renewables.

[2] Directive (EU) 2023/2413 of the European Parliament and of the Council of 18 October 2023 amending Directive (EU) 2018/2001, Regulation (EU) 2018/1999 and Directive 98/70/EC as regards the promotion of energy from renewable sources, and repealing Council Directive (EU) 2015/652

Solution

The Heating and Cooling Strategy should explicitly commit to a gradual but definitive phase-out of fossil fuels in the sector. This means not only ending new and already existing subsidies for fossil sources, especially fossil gas, but also implementing a timeline for their exclusion from the EU energy mix. A clear strategy to transition away from fossil fuels will enable Europe to accelerate the development of renewable solutions, generating economic benefits and improving social outcomes.

To unlock a meaningful shift across industries, the Heating and Cooling Strategy should also introduce a carefully designed target for renewable industrial heat to accelerate the phase-out of fossil fuels while preserving the competitiveness of European industries.

Actions

The revised Heating and Cooling Strategy should include clear phase-out timelines and require Member States to develop national roadmaps that outline:

- the planned reduction of fossil fuelled district heating systems,

- the deployment of renewable alternatives,

- and the necessary support measures for consumers and industries.

Supporting evidence #1 - GHG Redution

In the context of a 90% reduction in GHG emissions by 2040 and, further down, climate neutrality by 2050, phasing out fossil fuels should be a priority. Sectors such as agriculture, energy-intensive industries, and aviation will retain a significant share of residual emissions, even in ambitious scenarios. It is important to prioritise the sectors that are easier to defossilise.

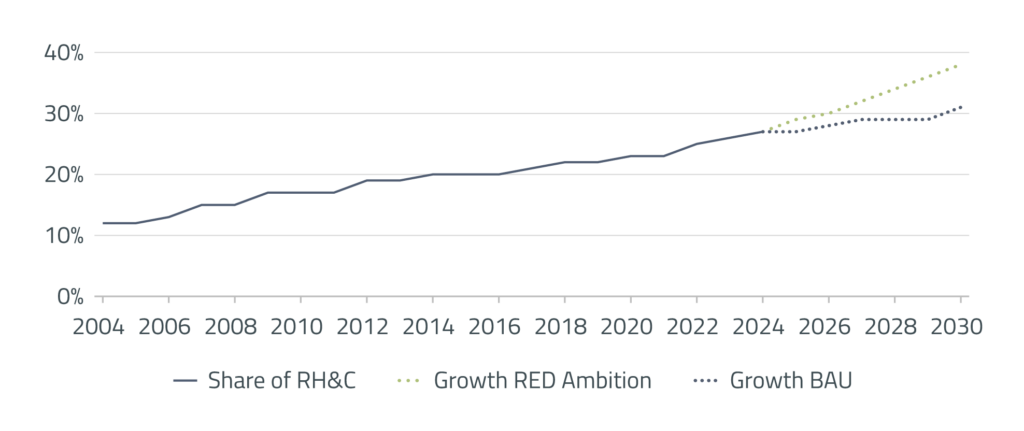

The figure below compares the recent evolution of the renewable share in H&C with two trajectories to 2030: business-as-usual (BAU) and the ambition implied by REDIII (+1.8 pp of yearly growth). The BAU line, extrapolated from historical data through 2024 using an exponential smoothing method, indicates that renewables in H&C continue to grow, albeit at a moderate pace. In contrast, the REDIII trajectory assumes an increase of around 1.8 percentage points per year and pulls away from the BAU curve.

This proves that relying solely on current trends will not be sufficient to meet the agreed-upon targets. The deployment of solutions such as sustainable bioenergy will be key to closing the gap between today’s progress and the renewable heating targets.

Supporting evidence #2 - Large-scale installations

Despite the gradual increase in renewables in H&C over the years, around 74% of the total heating supply in the EU is still provided by fossil fuels and nuclear power, meaning that millions of installations still rely on coal, gas, or oil.

This means there is substantial, relatively accessible potential for rapid emissions reductions through fuel switching, especially in large systems.

In industry and district heating, existing assets such as boilers or combined heat and power (CHP) plants can often be decarbonised without full replacement, for example by progressively co-firing sustainable biomass in coal units or by switching from natural gas to biomethane. Such conversions deliver steep reductions in the carbon footprint of the heat produced, while preserving the existing infrastructure.

This makes fuel switching one of the most cost-effective and operationally realistic levers to accelerate the decarbonisation of heating and cooling in the short- to medium-term.

Accelerate and support the replacement of outdated and polluting heating systems to meet the EU’s climate objectives and support citizens.

Problem

The European domestic heating systems are outdated, inefficient and polluting. In buildings, a large share of existing appliances not only underperform in terms of energy efficiency but also contribute significantly to greenhouse gas (GHG) emissions and poor air quality.[1]

[1] EC report N°ENER/C2/2014-641-2016

Solution

The revised Heating and Cooling Strategy should establish a framework to replace and modernise the existing stock, prioritising renewable solutions, such as sustainable bioenergy. New systems are highly efficient, capable of producing more heat using less feedstock, therefore reducing emissions and costs for consumers.

Actions

Dedicated national funds co-financed by the EU to support the replacement of obsolete appliances should be developed. It would deliver rapid emissions reduction while driving industrial innovation and job creation across the EU renewable heating value chain.

Supporting evidence #3 - The replacement challenge

The regulatory framework following the Heating and Cooling Strategy must be designed to drive much higher replacement rates.

This must be done not only through gradual efficiency improvements, but by terminating the placement on the market of new standalone fossil fuel boilers, as well as incentivising the replacement of the current stock.

To support the discussion, a stock model based on Eurostat data was developed by Bioenergy Europe to estimate the installed stock of coal, oil and gas boilers across EU Member States and the replacement rates required to phase them out by 2050[1].

The analysis indicates a considerable discrepancy between the current replacement rates, estimated at approximately 4% annually, and the level required to fulfil EU climate objectives. [2]

For example, in France, reducing the stock of gas boilers by around 90% by 2040 would require annual replacement rates of roughly 13%, about three times today’s levels. These findings highlight that achieving a credible phase-out of fossil fuel heating will require a regulatory framework that actively drives much higher replacement rates, including ending the placement on the market of new stand-alone fossil fuel boilers and strengthening incentives for stock replacement, supported by aligned national support schemes and renovation programmes.

[1] This stock model should be interpreted as indicative, order-of-magnitude-based rather than a precise inventory of heating appliances in the EU. It is based on household survey data reporting the main heating source per dwelling. In multi-dwelling buildings equipped with a single central heating appliance, this approach counts one appliance per flat, thereby overestimating the number of individual units installed. In addition, dwellings supplied by district heating are not captured in the survey.

[2] EHI, Decarbonisation pathways for the European building sector

Incentivise integrated planning to complement electrification with direct heat solutions.

Problem

Electrification will be key in a decarbonised future, but it cannot stand alone. Most renewable energy sources, particularly variable renewable electricity, are inherently intermittent and cannot fully respond to peak heating demand in winter. Relying solely on electrification will increase peak loads, system stress, and supply constraints, especially during cold periods when heat demand is at its highest.

For this reason, the continued use of biomass for heating helps alleviate electricity demand during peak hours, reduces grid stress, and improves overall system stability.

Solution

Bioenergy is already the single largest fuel used in European district heating (ahead of natural gas), with many cities across the EU relying on biomass-based district heating systems as the backbone of their heat supply. It is dispatchable, locally sourced, and essential for relieving electricity peak demand, rural heating, and hard-to-abate industries. It complements the EU’s electrification objective thanks to its flexibility and storage capabilities.

read more

Renewable-based district heating and poly-generation are allies of an ambitious Heating and Cooling Strategy. Delivering both heat and power helps decarbonise multiple sectors simultaneously. Leveraging existing fossil CHP assets by progressively increasing biomass co-firing rates is often the fastest and cheapest way to cut emissions, especially in coal- and gas-dependent district heating systems.

District heating networks also offer strong hybridisation potential, as large heat pumps can be coupled with bioenergy plants to capture low-temperature waste heat and reinject it into the network, boosting overall efficiency. Hybrid solutions are allowing the plant to be more flexible and to use electricity optimally when day-ahead prices are low due to high intermittent RES-e production.

Actions

The revised Heating and Cooling Strategy should explicitly recognise and integrate bioenergy as a complementary renewable solution to electrification. This should be reflected in system planning, peak demand management strategies and support mechanisms at the EU and national level. By promoting the coupling of different technologies in hybridised systems, we can maximise efficiency and utilise waste heat effectively. This not only applies to the electrification objectives but also ensures a more flexible and resilient heating network.

Supporting evidence #4 - 81% of renewable heating

Bioenergy accounts for 81% of renewable energy in the heating sector, and its share is even higher in renewable district heating, where it represents nearly 95% of the renewable energy mix. While its share may seem large, data shows that despite this strong contribution, fossil fuels, together with nuclear, still account for 73% of EU heating today, generating around 1.5 billion tonnes of CO₂ emissions each year.

This illustrates the untapped potential of the heating sector for renewable solutions such as bioenergy and highlights the need for a strategy that takes a technology-neutral approach, allowing local conditions in Member States to be properly assessed while accelerating the replacement of fossil fuels.

It is worth noting that biomass for heating is a cost-effective way to reduce CO2 emissions. A recent report from the Austrian Energy Agency confirms this information; for end users, replacing gas/oil boilers with woodchip or pellet systems often yields negative abatement costs. [1] From a public finance perspective, subsidising small and medium biomass systems for households and multi-family buildings ranges between 30 and 60€ per ton of CO2 saved. At the same time, large boilers and CHP plants fall within the 75-95 € per ton range. In a context of scarce budgets, directing the support to such low-cost CO2 reductions is essential to maximise climate impact per euro spent.

[1] Austrian Energy Agency, “CO2-reduction costs and potential of biomass-based heating systems compared to fossil and other renewable solutions”, Vienna, 2025.

Achieve meaningful yet achievable Ecodesign and Energy Labelling that considers affordability, ensuring a just transition for all.

Problem

The revision of Ecodesign and Energy Labelling requirements for solid-fuel local space heaters and boilers is crucial for the future of the sector and the EU’s decarbonisation pathway. If the new requirements are set too strictly or unrealistically, they will prevent the vast majority of systems from being commercialised in the EU market. This will eliminate a significant portion of the sector, consequently undermining European manufacturing, making the transition unaffordable for citizens and businesses, and hampering decarbonisation efforts.

Solution

Meaningful Ecodesign and Energy Labelling requirements are essential for EU competitiveness. A well-designed framework with ambitious yet realistic efficiency and emissions requirements can drive the development of better-performing technologies and support the transition to cleaner heating solutions.

Actions

The revised Ecodesign and Energy Labelling rules for solid fuel local space heaters and boilers should set forward-looking yet achievable limits that incentivise innovation and higher performance, while ensuring progressiveness that companies can adapt to, and that products remain affordable.

Favours “Made in EU technologies”, to promote innovation and manufacturing while boosting the EU industrial competitiveness and energy independence.

Problem

The European industry is not competitive enough. In the current geopolitical context, it is more important than ever to prioritise European technologies and the use of local resources. The energy crisis triggered by the Russo-Ukrainian conflict has shown that energy independence is a strategic priority that cannot be overlooked. Moreover, insufficient industrial incentives risk increasing reliance on non-European technology, moving from one dependency to another.

Solution

Technological neutrality and made-in-EU options should be prioritised to enable efficient solutions and support decarbonisation. European manufacturing should be actively incentivised to strengthen our industrial competitiveness and ensure that Europe maintains its leadership in the production of clean heating technologies.

Actions

The Heating and Cooling Strategy should actively link competitiveness, energy independence, technological neutrality and decarbonisation goals. In concrete terms, there should be regulatory support to incentivise European innovation and manufacturing and to preserve technological neutrality, thus strengthening the EU energy system.

Supporting evidence #5 - Bioenergy technologies

Europe is a global leader in bioenergy technologies, with over 50,000 companies and more than 800,000 jobs across the value [1]. Approximately 74% of equipment suppliers are European, and EU-made technologies are exported worldwide. This, combined with the fact that the EU has only a 5% import dependency on the biomass feedstock used, is a key competitive advantage for energy security and industrial competitiveness.

It is evident that the bioenergy sector serves as a significant catalyst for economic growth, innovation, and employment.

According to Deloitte, the sector’s contribution to the job market is projected to keep increasing, reaching nearly 1.5 million workers by 2050. Today, most of these jobs are in feedstock supply, but the focus is expected to shift towards higher-value activities, such as equipment manufacturing, engineering, and services. Manufacturing bioenergy boilers, stoves, CHP units, or fuel processing equipment is already a key part of the EU’s industrial portfolio, supported by European supply chains. By 2050, the sector’s contribution to EU GDP is expected to exceed €70 billion, with equipment manufacturing accounting for more than half of this value. This highlights the role of bioenergy as both a climate solution and a catalyst for industrial competitiveness and employment in the EU.

[1] Towards an integrated energy system: assessing bioenergy’s socio-economic and environmental impacts, Deloitte, 2022